Global logistics market forecast

The global logistics market is expected to grow at a CAGR of 6.8%1 during the period 2022-2030, especially due to the boom in e-commerce logistics, shortage of containers, closure of major ports causing port congestion, shortage of truck drivers, and constrained capacity in Air. Shipping market.

The Asia Pacific region will be the largest logistics market globally, holding nearly 45% of the total market share, and is expected to outperform other regions in the future due to the positive outlook for emerging economies in the region. Asia is expected to contribute about 50% of global trade growth by 2030.

Impact of e-commerce growth

With the omnichannel approach to retail e-commerce gaining ground, it has become imperative for logistics service providers to adopt automation and newer technologies like AI, geo-fencing, IoT and data analytics to make the delivery and returns experience seamless and cost-effective for both customers and retailers. The increasing adoption of analytics-driven dynamic route planning systems is facilitating logistics companies in optimizing operations and providing a cost-effective and seamless experience for both customers and retailers.

Impact of the Russian attack on Ukraine:

The conflict has disrupted supplies of key raw materials. The price of crude oil rose above $100 per barrel, causing the United States and other countries to withdraw oil from their emergency stockpiles. Shipments were redirected, derailed and suspended from surrounding areas, disrupting the global supply chain network.

The post-COVID-19 recovery will continue in 2022, and will accelerate over the next two or three years

Economic forecasts

Despite the threat posed by the Omicron variant, the outlook for the global economy in the near term is positive. Real GDP growth is expected to continue at more than 3.9% year-on-year in 2022, driven by continued expansions in the United States and Asia4.

Ongoing pandemic-related delays and closures, high demand for ocean freight from Asia to the United States, and capacity constraints have led to high prices and unreliable transit times for air and sea freight, but resuming full operations at China’s Yantian Airport will ease pressure on the logistics industry. .

Shipping rates

Strong consumer demand, new pandemic-related restrictions and container capacity shortages, which are expected to persist through 1Q22, are likely to keep freight rates high in all geographies.

Environmental, Social and Governance Risk Framework

Amid increasing pressure from customers, employees, regulators and investors, transportation and service providers are prioritizing adopting more sustainable processes to align with evolving market realities and gain a competitive advantage. However, there are only a few companies that have embraced these processes.

Workforce diversity

Workforce diversity in the transportation and logistics (T&L) industry lags significantly behind other industries; Hence, industry players (such as DHL, Maersk and XPO Logistics) are prioritizing the adoption of policies that ensure diversity and inclusion within their workforce.

Challenges

The shortage of shipping containers (a “black swan” event) is emerging as a serious concern as demand for Asian exports increases strongly, filling all available ship capacity and leaving equipment stranded in the US and EU.

Port congestion, especially along the West Coast of the United States, has proven to be a major problem for shipping companies, as ships now have to wait longer to unload their cargo, leading to higher costs.

As demand for logistics services and labor shortages increase due to the pandemic, there is increasing pressure on labor supply, especially in the trucking industry, which is facing a significant driver shortage.

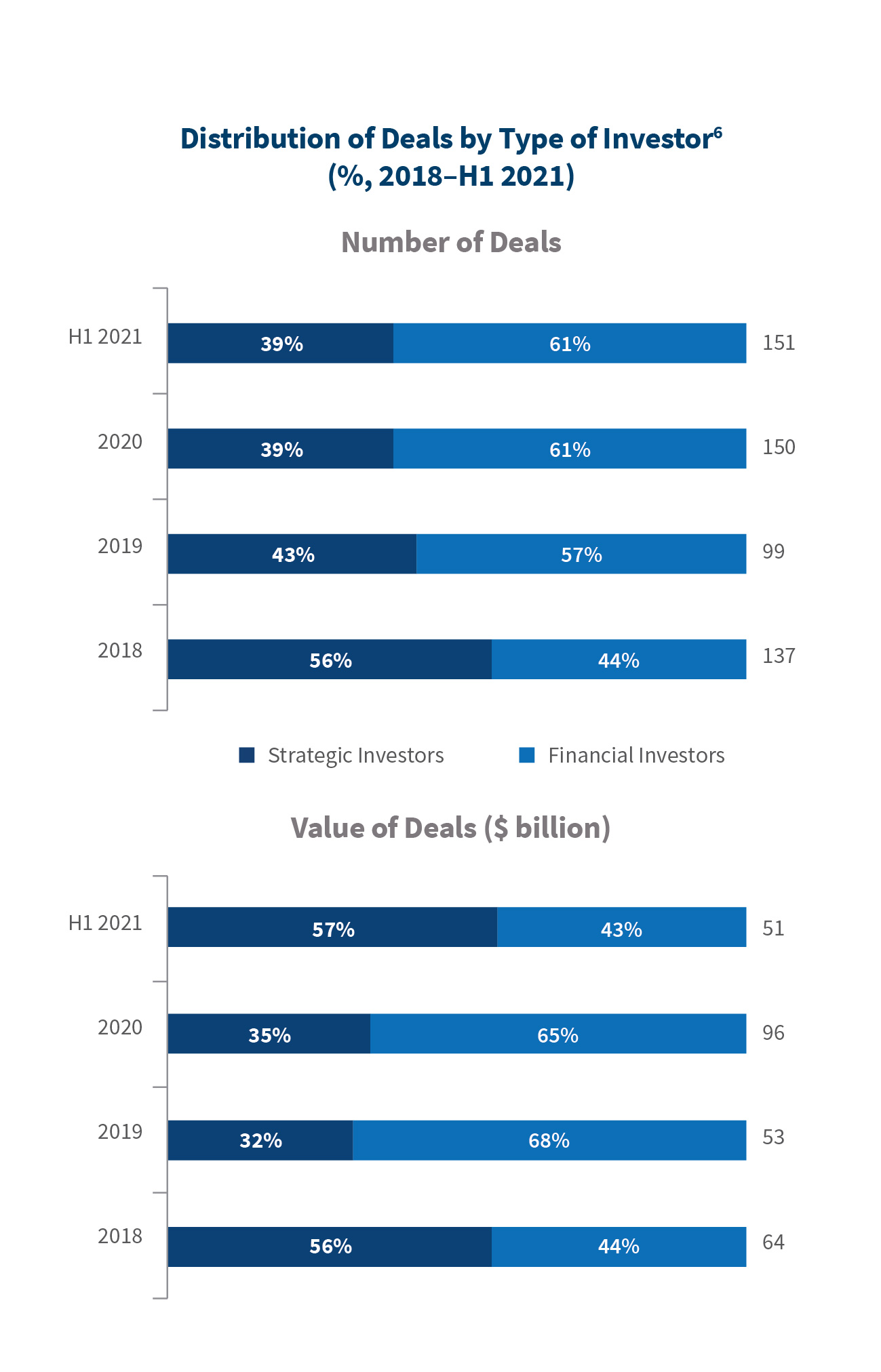

Investments and bankruptcy

Mergers & Acquisitions Trends: Deal value through November 15, 2021 was up 84% compared to the previous year, driven primarily by deals in the logistics, rail and passenger aviation sectors. Growth in deal volume increased by 11% compared to FY20 due to increased deals in the vehicle leasing and leasing, logistics and trucking segments.

Private Equity Investments: Private equity firms saw a 21.9% increase in deal value during the first five months of 2021, resulting in a total of 2,346 deals.

Private equity firms are raising money faster due to higher fund counts and institutional investor allocations; This led to an all-time high in dry powder of $920 billion in October 2021.

Bankruptcies: Instability caused by the pandemic led to extreme fluctuations in demand, prices and capacity, resulting in the bankruptcies of thousands of truck carriers, a decline in intermodal demand, and a 12% reduction in the number of railcar loads.

About 3,000 trucking companies had to close their businesses in 2020 due to the pandemic, compared to 1,000 in 2019.